Buying Property with Family or Friends: Your 2025 Guide to Co-Ownership in Australia

Unlock the benefits, navigate the risks, and understand the essential legal structures for successfully purchasing real estate with a partner.

Introduction

Navigating the Australian property market in mid-2025 presents a significant challenge for many aspiring homeowners and investors. With property prices remaining high, the dream of securing a desirable asset can feel out of reach. This has led to a surge in a popular strategy: co-ownership, or buying property with friends, siblings, or other family members. By pooling resources, buyers can enter the market sooner and purchase a more valuable property than they could alone. However, this path is filled with potential financial and personal pitfalls. This comprehensive guide will break down the complexities of co-ownership, from legal structures and lending hurdles to the critical importance of a rock-solid exit strategy, empowering you to make an informed decision.

The Primary Advantage: Boosting Your Buying Power

The most compelling reason for co-ownership is the immediate boost to your purchasing power. For many, the biggest obstacle to entering the property market isn't servicing a loan, but saving the substantial deposit required. Let's consider a common scenario: you have saved $30,000, which severely limits your options. Meanwhile, your sibling or a close friend has saved $100,000. By combining your funds, you can suddenly target a more premium property in a location with better long-term capital growth prospects.

This strategy allows you to:

Enter the Market Sooner: Instead of spending years saving while the market potentially moves further away from you, co-ownership provides a fast track to getting your foot on the property ladder.

Purchase a Better Asset: A larger combined deposit means you can afford a better quality property, whether that's a house instead of an apartment, a more desirable suburb, or a property with development potential.

Share Ongoing Costs: Mortgage repayments, council rates, insurance, and maintenance costs are all split, reducing the ongoing financial burden on each individual.

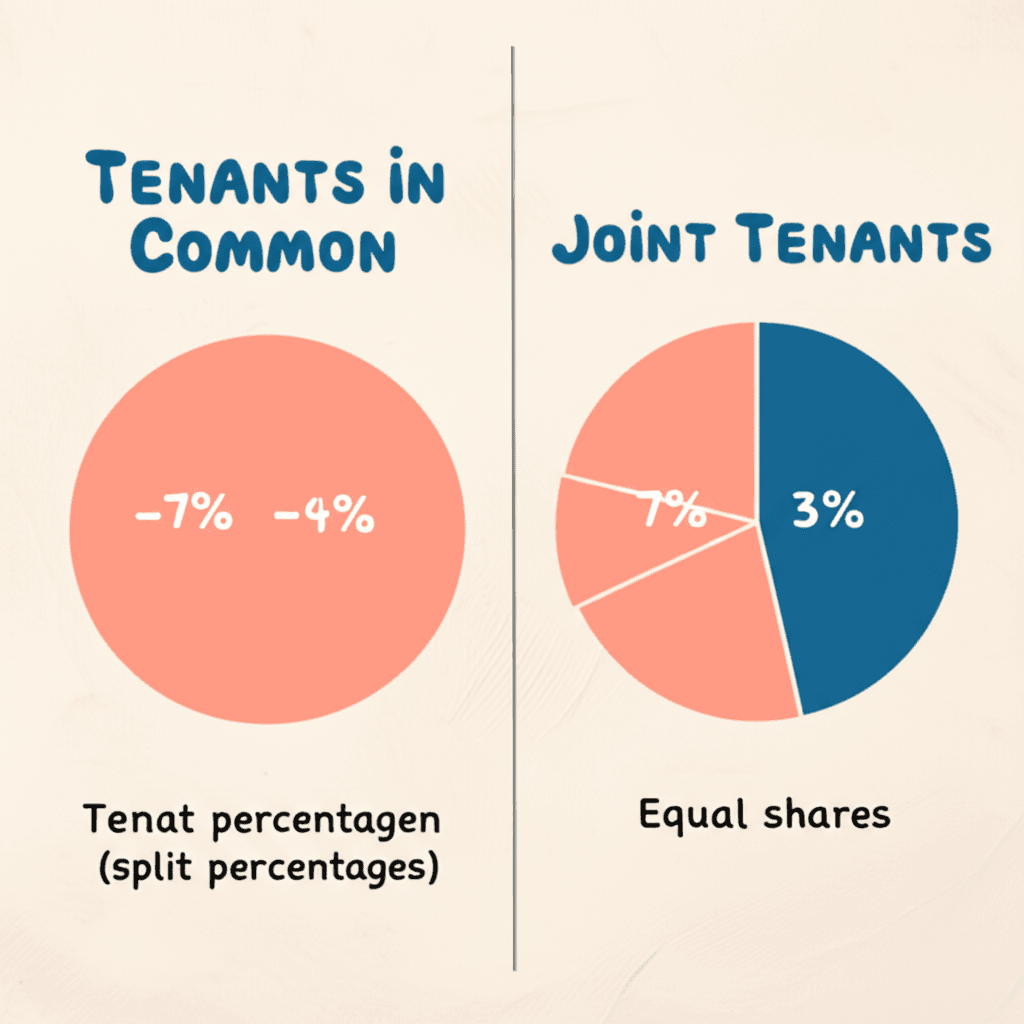

Understanding the Legal Framework: Tenants in Common vs. Joint Tenants

When you buy a property with someone who isn't your spouse, setting up the correct legal ownership structure is non-negotiable. This is where you'll need professional legal and accounting advice. The two primary structures in Australia are Joint Tenants and Tenants in Common.

Joint Tenants

This is the most common structure for married couples. Under a Joint Tenancy, all owners have an equal, undivided share in the property. The defining feature is the 'right of survivorship'. If one owner passes away, their share automatically transfers to the surviving owner(s), regardless of what is stated in their will. This structure is inflexible for co-buyers who are contributing different amounts.

Tenants in Common

This is the recommended structure for non-spousal co-ownership. Tenants in Common allows for unequal ownership shares, which is crucial when partners contribute different amounts to the deposit. For instance, one person could own 60% of the property while the other owns 40%.

Key benefits of Tenants in Common include:

Unequal Shares: Ownership can be split in any proportion (e.g., 70/30, 99/1) to reflect each person's financial contribution. This is also useful for tax purposes, allowing the higher-income earner to claim a larger portion of the tax deductions from negative gearing.

No Right of Survivorship: Each owner's share is treated as a separate asset. If one owner passes away, their portion of the property is distributed according to their will, not automatically passed to the other co-owner.

Individual Financial Control: It forms the legal basis for separating the debt, which is a critical component of a sophisticated co-ownership strategy.

Navigating the Financial Maze: Lending and Future Borrowing Capacity

Securing a loan for a co-owned property is straightforward, but the real challenge emerges when one partner wants to buy another property in the future. This is where many co-ownership arrangements derail personal portfolio growth.

The Initial Loan and Property Share Arrangements

Some lenders offer specialised 'property share' loans that align with a Tenants in Common structure. In this setup, each co-owner is responsible for their portion of the debt. For example, if you own 40% of a $600,000 property with a total loan of $480,000, your individual loan would be $192,000 (40% of the debt). This loan can appear separately on your internet banking, and you can even have your own offset account against it. However, it's vital to understand that you will almost always be required to act as a guarantor for your partner's portion of the loan. If they default, the lender can pursue you for the entire debt.

The Future Borrowing Trap

Here lies the biggest financial risk. Years later, your income has increased, and you want to buy a home with your new partner or expand your investment portfolio. When you apply for a new loan, many lenders will assess your serviceability by taking 100% of the co-owned property's debt but only considering your 40% share of the rental income. This can drastically reduce your borrowing capacity and halt your investment journey.

To overcome this, you must seek out a lender with a 'non-spousal common debt reducer' policy. Only a handful of lenders in Australia have this policy, which allows them to consider only your actual portion of the debt in their serviceability calculations. This severely limits your lender options for future purchases, potentially forcing you into less competitive interest rates. That's why getting expert guidance through our AI Buyer's Agent can be invaluable in planning your long-term strategy from day one.

The Hidden Risks: Beyond the Finances

Buying property together is like entering a business partnership or a marriage. Success depends on trust, communication, and aligned goals. Before you sign anything, you must consider the personal risks.

Mismatched Financial Habits: What if you are a diligent saver, but your co-owner is frivolous with money? When a $10,000 repair bill for a new roof arrives, will they have the funds, or will the burden fall entirely on you?

Life Changes: Life is unpredictable. One person might get married, have children, lose their job, or want to move overseas. These events can trigger a need to sell the property at an inconvenient time.

Disagreements on Property Management: You need to agree on everything, from selecting a tenant and setting the rent to approving maintenance requests. A simple disagreement can strain the relationship.

If you can afford to buy a property on your own, it is almost always the simpler, less risky path. It provides you with complete control and avoids the complexities that can strain even the strongest friendships and family bonds. However, if co-ownership is your only viable path, meticulous planning is essential.

The Golden Rule: A Watertight Co-Ownership Agreement and Exit Strategy

The single biggest mistake co-owners make is failing to plan for the end of the partnership from the very beginning. A verbal agreement is not enough. You need a legally drafted co-ownership agreement that clearly outlines the exit strategy.

Most people create an open-ended agreement, assuming they'll figure it out when someone wants to leave. A far better approach is to plan for a short-term venture (e.g., 3-5 years). At the end of this term, you are forced to re-evaluate. The agreement should only be extended if all parties explicitly agree to continue.

Your agreement should cover:

The Exit Plan: How will the partnership end? Will the property be sold on the open market? Does one partner have the first right to buy out the other, and how will the valuation be determined?

Financial Contributions: Detail all initial contributions (deposit, stamp duty, legal fees) and how ongoing expenses will be paid.

Default Scenarios: What happens if one person can't make their mortgage repayments or contribute to a major repair?

Dispute Resolution: Outline a process for resolving disagreements.

Conclusion: A Powerful Tool When Used Wisely

Co-owning property can be a brilliant strategy to accelerate your entry into the Australian real estate market. It can unlock opportunities that would otherwise be out of reach. However, it is a high-stakes venture that demands more than just a combined deposit—it requires legal protection, financial foresight, and a bulletproof exit plan. By structuring the ownership as Tenants in Common and creating a comprehensive legal agreement from the outset, you can mitigate the risks. Treat it as a business transaction, have open and honest conversations, and always plan for the end before you even begin. To navigate these complexities and ensure your property journey aligns with your long-term goals, explore how the guided process of HouseSeeker's [AI Buyer's Agent](https://houseseeker.com.au/features/ai-buyers-agent) can provide the clarity and strategic direction you need.

Frequently Asked Questions

What is the biggest risk of buying property with a friend?

The biggest financial risk is the negative impact on your future borrowing capacity, as many lenders will hold you liable for the entire property debt. The biggest personal risk is a breakdown of the relationship due to disagreements over money, property management, or a change in life circumstances that forces a premature sale.

Why is 'Tenants in Common' better for co-buying with family or friends?

Tenants in Common is superior because it allows for unequal ownership shares that reflect each person's financial contribution. Crucially, it does not have a 'right of survivorship', meaning each person's share can be passed on according to their will, providing essential asset protection.

Should our co-ownership agreement be in writing?

Absolutely. A verbal agreement is unenforceable and a recipe for disaster. A legally drafted co-ownership agreement is essential. It should detail all financial arrangements, responsibilities, and, most importantly, a clear exit strategy that outlines how and when the partnership can be dissolved.