A Strategic Guide to Acquiring 10 Investment Properties in 3 Years

Learn the deposit recycling strategy to leverage an initial $100k investment into a substantial real estate portfolio.

Introduction

Building a substantial property portfolio can seem like a long-term game, but with the right strategy, it's possible to accelerate your journey. This guide explores an aggressive investment model: how to potentially acquire ten properties in just three years, starting with $100,000 in savings or equity. This method, known as deposit recycling, focuses on strategic acquisitions and leveraging equity to rapidly scale your portfolio. While this is a powerful technique, it requires discipline, careful planning, and a deep understanding of market dynamics.

Disclaimer: The following content is for informational purposes only and does not constitute financial advice. We recommend consulting with a qualified financial advisor and mortgage broker before making any investment decisions.

The Three Pillars of a Rapid Growth Strategy

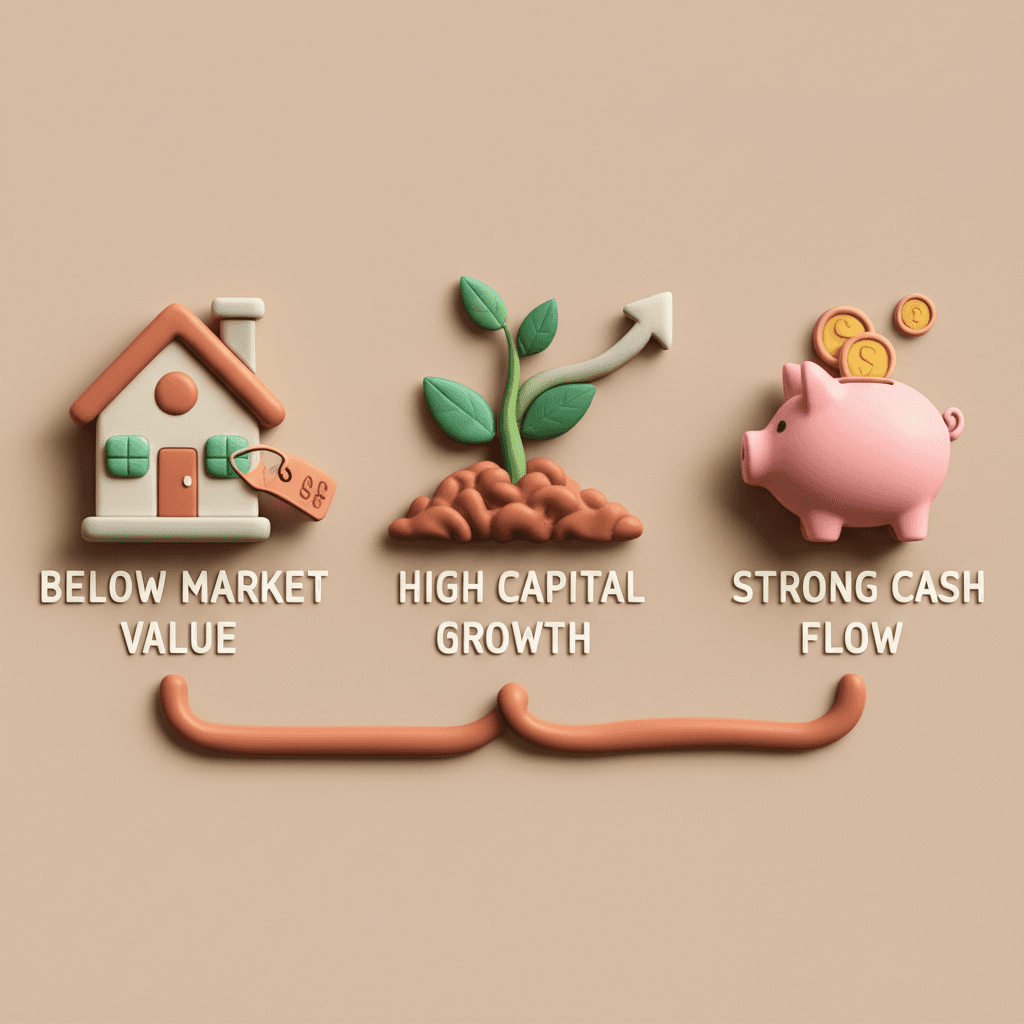

This strategy is built on a foundation of three critical property selection criteria. Success depends not just on recycling capital, but on the quality of the assets you acquire. Each property must tick these three boxes to ensure the portfolio is both scalable and resilient.

1. Buy Below Market Value: The core of this strategy is manufacturing equity from day one. By purchasing a property for 10-20% less than its current market worth, you create an immediate equity buffer. This makes it possible to refinance sooner and extract your initial deposit without waiting for market-driven capital growth. 2. Target High Capital Growth: Your properties must be located in metro areas poised for significant growth. Analysing market cycles and identifying suburbs with strong growth drivers is essential. Tools that provide deep real estate analytics are invaluable for pinpointing these high-performing markets. 3. Prioritise Strong Cash Flow: Each property must have a high rental yield (aiming for 6% or more) to ensure it is cash-flow positive or at least neutral. This strong cash flow helps service the loans, covers expenses, and improves your borrowing capacity for future purchases.

The Deposit Recycling Method: A Step-by-Step Breakdown

With the foundational principles established, here is how the strategy unfolds over a three-year timeline.

The journey begins by splitting your initial $100,000. You'll allocate approximately $50,000 for each of the first two properties. For a $300,000 property, a 10% deposit ($30,000) plus costs like stamp duty and legal fees will use up most of this initial allocation.

After an initial period of 6-8 months, you work with your mortgage broker to get these properties revalued. Because you purchased them below market value (e.g., bought for $300k, now valued at $350k-$360k), you can refinance to a new 90% loan-to-value ratio (LVR). This process effectively extracts your original ~$50,000 deposit from each property, giving you back your initial $100,000 to reinvest. You then use this recycled capital to purchase two more properties, bringing your portfolio to four properties by the end of the first year or early in the second.

After another 3-6 months, you repeat the refinancing process on your third and fourth properties. With the extracted $100,000, you can now scale more efficiently. Instead of two separate houses, consider purchasing a duplex for around $600,000. A duplex provides two separate rental incomes on a single title, significantly boosting your cash flow and simplifying management. This single purchase adds two more properties to your portfolio, bringing the total to six.

As you enter the final phase, the cycle continues. Refinance the duplex once sufficient equity is established and use the released funds to purchase another two properties. This brings your count to eight. For the final push, a delayed refinance on one of the earlier properties or the purchase of another duplex can help you reach the goal of ten properties within the three-year timeframe.

Navigating Financial Hurdles

Rapidly acquiring properties presents unique challenges, particularly concerning borrowing capacity. As your portfolio grows, you may need to move from major banks to second and third-tier lenders who have different lending criteria. This requires a strategic approach guided by an experienced mortgage broker.

Furthermore, this strategy is not a purely passive one. It can be challenging and time-consuming, and having the right team is crucial. A skilled professional, like an AI Buyer's Agent, can help source properties that meet the strict criteria required for this model to succeed.

Conclusion

Acquiring ten properties in three years with a $100,000 start is an ambitious but achievable goal for a determined investor. The strategy hinges on the disciplined execution of buying undervalued, high-growth, cash-flow positive assets and strategically using refinancing to recycle your initial capital. It requires a strong team, a persistent mindset, and the willingness to navigate complex financing hurdles. While this model can fast-track wealth creation, it also highlights the power of leveraging data and expert guidance to make smart, calculated investment moves.

Ready to find your next high-performing investment? Use HouseSeeker's Real Estate Analytics to uncover market trends, identify growth suburbs, and make data-driven decisions.

Frequently Asked Questions

What is the biggest risk with this strategy?

The primary risks include market downturns that prevent capital growth, valuations coming in lower than expected, or an inability to secure refinancing. These risks are mitigated by the core principle of buying significantly below market value, which creates an instant equity buffer, and by focusing on properties with strong cash flow to ensure they remain financially stable even if interest rates rise.

Is paying Lenders Mortgage Insurance (LMI) bad in this model?

Not necessarily. While LMI is an added cost, in this strategy, it's treated as a tool to achieve leverage and speed. Paying LMI allows you to use a smaller deposit, get into the market faster, and begin the equity recycling process sooner. The goal is for the manufactured equity and capital growth of the property to far outweigh the initial cost of LMI.

Can I execute this strategy without a buyer's agent?

While it is possible, it is extremely challenging. The success of this entire strategy depends on consistently finding properties 10-20% below market value that also meet strict growth and yield criteria. This requires extensive market knowledge, a strong network, and significant time. Services like HouseSeeker's AI Property Search can help identify opportunities, but the expertise of a dedicated agent is often invaluable for negotiation and off-market access.